As the economic recovery in Malaysia continues apace in 2022 after two years of being ravaged by the COVID19 pandemic, we are facing many domestic as well as international challenges. On the whole, I am quite bullish about the trajectory of the Malaysian economy in the new few years, especially in the context of ASEAN which will continue to see an influx of Foreign Direct Investment (FDI) from the EU, US and later on, from China (when it eventually re-opens its borders). In the meantime, there are many domestic policy issues which we need to manage well so that we can maximize the upside for our economic recovery and reposition the various sectors of our economy to take full advantage of regional and global trends. Managing the economy is a complex task requiring policy understanding and coordination on the part of various stakeholders including Members of Parliament. Since this task cannot be condensed to a few short paragraphs in one press statement, I am beginning a series of articles entitled “Managing the Economy” where I will flesh out my thoughts on how we can better structure and align our policies to push full steam ahead in our economic recovery.

This first article focuses on two related areas which have been the subject of domestic as well as international attention namely – inflationary pressures and disruptions in the supply chain. We start with the Consumer Price Index (CPI) which is the commonly used index to measure domestic inflation. The problem with ONLY using CPI as a reference point to understand inflationary pressures in the country is that many of the items in this index comprises of controlled price items such as chicken, electricity, and petrol prices. For example, the Minister in charge of the Economy in the Prime Minister’s Department, Mustapha Mohamed, referred to the March CPI figure of 2.2% year on year inflation rate to show that inflation was still low and under control. While his statement is “technically” correct, it fails to demonstrate an understanding of the tremendous upward cost pressures which different supply chains in the country are facing.

We just need to examine in greater detail the upward pressure on food and non-alcoholic beverages where the inflation rate was 4.0% and 4.1% in March and April 2022. Within this category, there are several essential items which have seen price increased, based on statistics collected by the Department of Statistics Malaysia (DOSM), which far exceed 4.0%. For example, the price of 3kg of cooking oil has increased by 37.2% from April 2021 to April 2022, the price of Grade A eggs has increased by 22.7%, the price of Sweetened Creamer (500 grams) has increased by 18.9% and even the price of 1kg of chicken has increased by 10.7% over this time period (Table 1 below).

Table 1: Change in Price (Absolute and %) on selected Food related items (April 2021 to April 2022)

|

All prices in RM |

Cooking Oil 3kg |

Sweetened Creamer 500gm |

Grade A Eggs |

Chicken |

|

Apr-21 |

18.52 |

2.75 |

3.65 |

8.58 |

|

Apr-22 |

25.41 |

3.27 |

4.48 |

9.50[1] |

|

Change in Price |

6.89 |

0.52 |

0.83 |

0.92 |

|

% Change in Price |

37.2% |

18.9% |

22.7% |

10.7% |

[1] Even though the ceiling price for 1kg of chicken was set at RM8.90 by the Ministry of Domestic Trade and Consumer Affairs, DOSM list the average selling price per kg of chicken in Malaysia at RM9.50 in the April 2022 CPI report.

Source: Consumer Price Index (CPI) April 2021 and April 2022 Reports

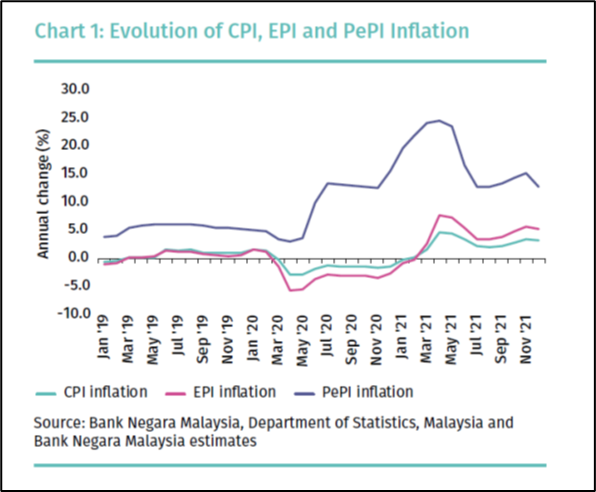

Even Bank Negara has acknowledged the need to look beyond the CPI to gauge the increase in prices which more accurately represented what people are “feeling on the ground”. In the 2021 Bank Negara Annual Report, two alternatives to the CPI namely, the Everyday Price Index (EPI) and the Perceived Price Index (PePI), were shown to be higher than the traditional CPI calculations (Chart 1 below).

According to Bank Negara’s calculations, the annual change in the CPI was 2.1% from 2010 to 2019 as compared to 2.6% for the EPI and 7.5% for the PePI during the same time period! In other words, the perceived inflation rate was 3 times that of the inflation rate calculate by the CPI! From Chart 1 below, we can observe that the divergence between the PePI and the CPI started increasing since May 2020 and this gap has persisted until now.

Source: Bank Negara Annual Report 2021

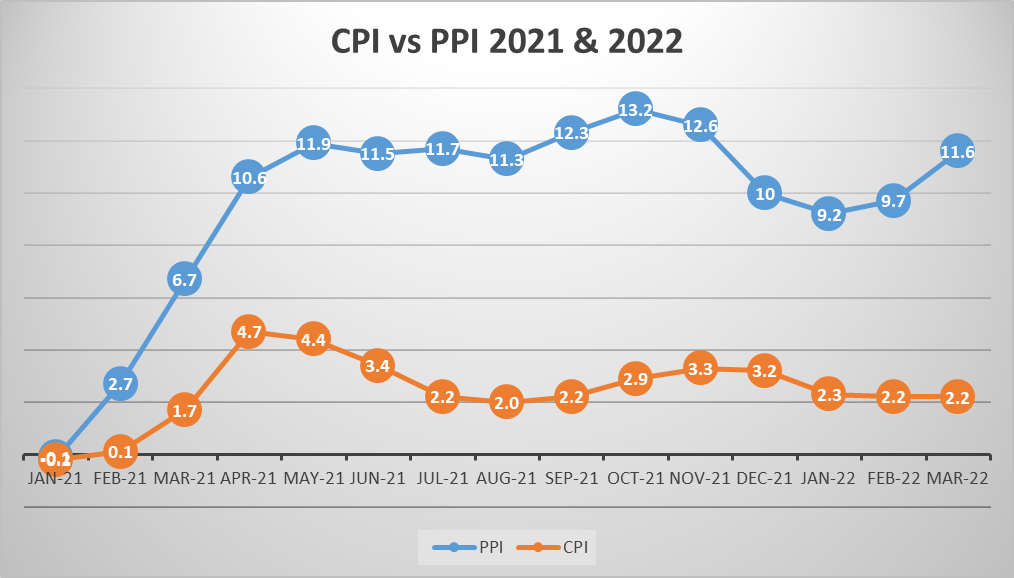

A more accurate picture of the upward cost pressures is the Producer Price Index (PPI) which covers the cost of production of five main sectors of the economy namely Agriculture, Forestry and Fishing; Mining; Manufacturing; Electricity and Gas Supply; and Water Supply. While the prices of many of the goods in the CPI are controlled, there are less of such controlled price items in the PPI. The increases in the cost of production will either be absorbed by the producers, be subsidised by the government either in part or in full or be passed down to the consumer. In 2021, many businesses would have been hesitant to pass down a significant portion of the cost increases to the consumer either because they had to fulfil their contracts based on previously agreed on prices or because of fears of weak consumer demand since the country was still in the thick of the pandemic. In 2022, with the economy in full recovery mode, businesses will have to pass on most of the cost increases to the consumer especially since most products are not subsidised by the government.

The PPI registered increases of 9.2%, 9.7% and 11.6% in January, February and March 2022 as compared to the CPI increase of 2.3%, 2.2% and 2.2% during the same period. With the war in Ukraine not showing any signs of ending soon and continued supply chain disruptions arising from various sources including the unexpected city and provincial lockdowns in different parts of China, and the expected impact of the minimum wage in Malaysia kicking in starting in May 2022, the PPI will likely register double digit increases for the rest of 2022 which means that upward pressure of costs and overall prices will also continue unabated.

Chart 2: Consumer Price Index (CPI) vs Producer Price Index (PPI) Jan 2021 to March 2022 (PPI for April 2022 has not been published yet)

Source: Department of Statistics Malaysia (DOSM)

To make matters worse, the PPI does not even cover other areas and sectors which have experienced and are experiencing significant cost increases including the logistics and construction sectors, agricultural products not produced in Malaysia, commodities which are not produced or mined in Malaysia such as copper and different parts of the services sector such as F&B and retail.

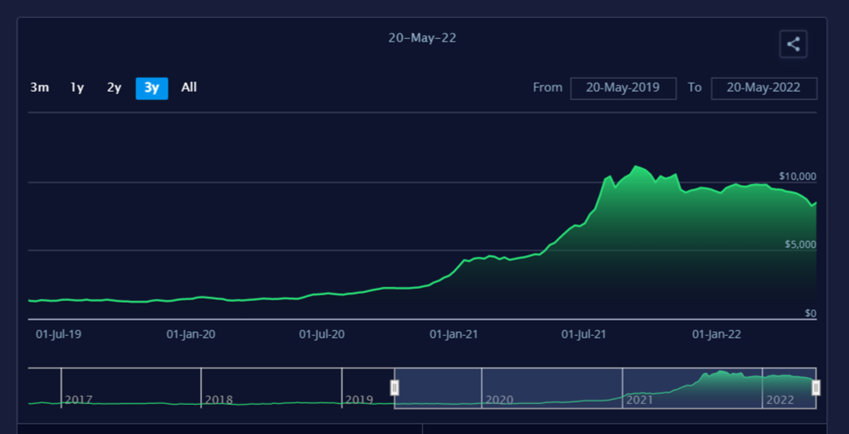

For some of these sectors, it is useful to look at global trends in prices as an indicator on the impact to the Malaysian business community and domestic consumers. For example, the Global Container Freight Index (also known as the Freightos Baltic Index or FBX) shows the daily pricing for the cost of shipping 40-foot containers on 12 global trade lanes (Chart 3 below).

Chart 3: Three Year Trend for Global Container Freight Index (Freightos Baltic Index FBX)

Source: https://fbx.freightos.com/

The FBX experienced a significant increase in the middle of 2021 as the various stimulus packages in the US and the EU resulted in increased consumer spending on goods such as electronic items. This index hit a high of more than US$11,000 in September 2021 before falling back to below US$10,000. The current price of US$8400 is still higher seven times higher than what it was back in May of 2019.

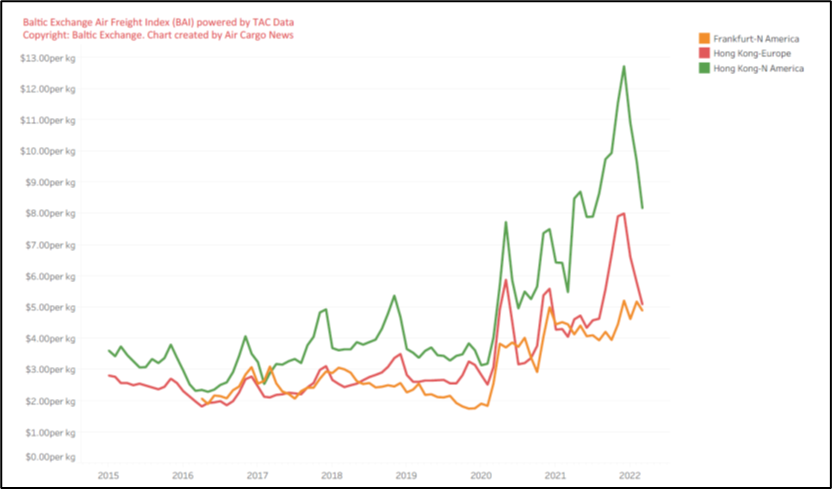

Chart 4 below shows the trend in air freight prices as measured by the Baltic Air Freight Index (BAI Index) which is a weighted average of 17 underlying destination basket routes for major airport destinations around the globe. Air cargo freights started increasing in 2020 because of the decrease in air passenger traffic (since these passenger planes also carry cargo). It hit a high of close to US$13/kg at the end of 2021 for the Hong Kong-North America route before falling back to the current US$8/kg, as passenger air traffic has started to increase.

Chart 4: Seven-year trend of the Baltic Exchange Air Freight Index

Source: https://www.balticexchange.com/en/data-services/market-information0/air-freight-services.html

There are many indexes which track the changes in the price of different baskets of commodities globally. One such index is in the Dow Jones Commodity Index (DJCI) which is a weighted index that tracks a wide range of 28 different community futures contracts including copper, cattle, wheat, soya, coffee, and oil and gas. Such an index gives us a better idea of global commodity prices as a whole. It is a useful guide for policymakers, but it is also necessary to look into individual commodity prices such as wheat and soya if we want to better understand and estimate the change in prices for items as such animal feed which is used to feed chickens in Malaysia, for example.

The DJCI has been slowly increasing at the start of 2022 and experienced a sudden upward spike in February, when Russia invaded Ukraine. At the 1200 level where it is currently hovering, the DJCI is 30% higher than what it was in December 2021.

Chart 5: One Year trend in the Dow Jones Commodity Index (DJCI)

Source: https://www.cnbc.com/quotes/.DJCI

Malaysia, being an open trading nation, with a high exposure to many imported items across the supply chain, will definitely be exposed to changes in the global cost of transportation and also the cost of commodities, either directly through our purchases of metals such as copper and steel and indirectly through our purchases of items which such as animal feed which is used to feed chickens and pork. We cannot afford to “hide” behind our low inflation figures and think that our businesses will only have a limited exposure to such global trends. This is one of the reasons why I find it totally unhelpful when some Ministers compared our “low” inflation rate to the “high” inflation rates in the United States and the EU because this kind of attitude allows the Malaysian government to ignore many of the inflationary pressures and supply chain challenges faced by the various business in the country until the situation become critical such as the chicken shortage we are currently facing.

The government’s policy on the domestic supply of chickens and chicken eggs is a microcosm on the failure to understand and act on the cost pressures our suppliers are facing because of global factors such as the increase in the price of animal feed and local factors such as the inability to hire workers, especially foreign workers, for the manual jobs which locals do not want to fill. Even with the subsidy of RM0.60 sen per kg which was announced in February 2022, the suppliers were already warning about future disruptions in the supply of chickens and eggs. If the suppliers could not cope with rising chicken feed prices, without a sufficient subsidy from the government, the inevitable outcome would be a reduction in how much grains the chickens would be fed leading to the chickens being underweight or taking too long to grow to the ‘right’ size. This is exactly what happened which led to the temporary suspension of the sale of chickens by some of the major poultry producers in Malaysia.

The announcement by the Prime Minister earlier this month to abolish Approved Permits (APs) for most food imports including chicken would not necessarily solve our chicken shortage problem. Apart from some of the longer term negative economic consequences on local producers, local supermarkets have to compete with other countries which are also sourcing for their own chicken supplies. In addition, according to the Ministry of Agriculture and Food Industries (MAFI), import permits are still needed at the border even though APs are no longer needed. Furthermore, sources for imported chicken are limited by the halal certificate requirement, a process which often takes years to certify. Ironically, the decision to ban the exports of chickens , which may look like a workable short term solution, will end up hurting local chicken producers and even chicken imports for the following reasons: (i) This will decrease the level of cross-subsidy available to local chicken farmers since they can earn more from their export sales to countries in like Singapore (ii) Local chicken farmers may have to pay compensation because of possible breach of contractual obligations to their overseas customers and (iii) Many of the countries which import from Malaysia will be forced to look for other supply sources in the region and they will be able to offer better prices compared to Malaysian retailers who are looking to diversify their own import sources!

Recommendations

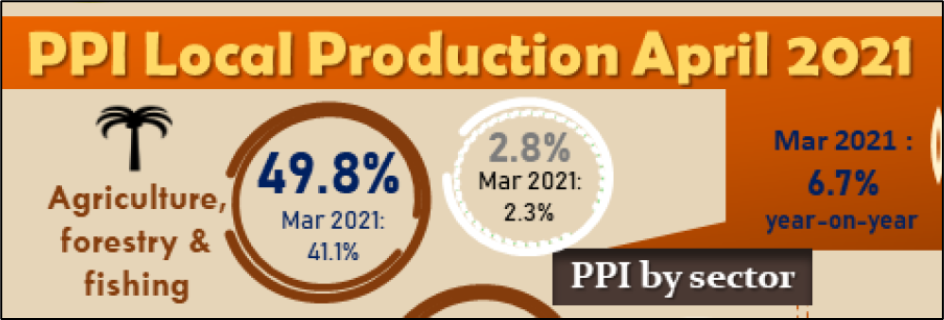

What should the government have done? Firstly, the Ministry of Agriculture (MAFI) should have announced a comprehensive approach towards addressing the food security issues in the country in 2021 once inflationary trends were being felt, domestically and internationally. They should have worked with DOSM to better explain the cost pressures being faced by domestic producers as part of a process to prepare the public for a possible future increase in the price of chicken and other food items. For example, the PPI for Agriculture, Forestry and Fishing in March and April of 2021 was already recording increases of more than 40% (See Chart 6 below). Back in 2021, MAFI could have started planning a strategy of diversification of our food import sources. We can take lessons from the Singapore Food Authority which has already put a plan in place to diversify their food import sources to over 170 countries as of 2019. MAFI should also have worked with the Ministry of Home Affairs and Ministry of Human Resources to expedite the processing of foreign workers for chicken producers which would have been helpful to increase production when needed. I believe that MAFI already has published many documents to chart the course towards greater food security in the medium to long term but most of these plans have not been followed through.

Chart 6: PPI Local Production April 2021 for Agriculture, Forestry and Fishing

Source: PPI report, April 2021

What is most disappointing to me is that MAFI has not issued any press statements either by the Minister or the Deputy Minister to address the current food price and food security challenges being faced. The latest activity in terms of public communications on the MAFI website was to announce the Hari Raya open house with the Minister on the 24th of May 2022! Similarly, the National Action Council on Cost of Living Action Council (NACCOL), of which the Ministry of Domestic Trade and Consumer Affairs is the secretariat, has not published any press statements or plans to address the larger cost of living issues and inflationary pressures being felt in other sectors of the economy!

Since these inflationary pressures will be present for the remainder of the year and perhaps beyond, some of the lessons learned from the chicken fiasco can still be put in place for other sectors of the economy. My recommendations to the government include the following:

- Each Ministry should publish their own index of producer and consumer costs based on the economic sectors and activities which come under their purview. Obviously, Ministries with more involvement in economic activities such as Finance, MITI, Agriculture, Transportation, Domestic Trade and Consumer Affairs, Communications (via Ecommerce), Energy, Works, Local Government and Housing and Tourism. But even other Ministries which are less “output” inclined also need to think about costs. For example, the Ministry of Women, Family and Community Development must keep track of the costs being faced by childcare centers as a result of increasing food costs and the cost of hiring carers. There should be a separate index for each Ministry to track the producer and consumer costs for Sabah and Sarawak. Each Ministry must work with DOSM to analyse existing data and to collect additional data if and when needed.

- The Ministries which currently sit in NACCOL should prepare a resiliency plan for key economic sectors including alert levels for possible supply chain disruptions instead of tackling the crisis only when the situation becomes untenable. This will force the Ministries to do scenario planning early and be prepared for different possible outcomes for different sectors of the economy. These resiliency plans must include identification and diversification of import sources for the raw materials which are important to different sectors of the economy.

- There must be inter-ministerial cooperation to address these issues rather than each Ministry working in silos. For example, MATRADE, an agency under MITI, should use its local and global network to work with MAFI and MDTCA to diversify food import sources.

- The Ministry of Home Affairs and the Ministry of Human Resources must publicly announce their KPIs for the processing of foreign worker visa applications for each sector of the economy as a way to alleviate supply chain and cost pressures being faced by businesses as the domestic, regional and global economy continues to open up.

- Finally, there must be proper communications including press briefings and press statements and social media outreach by the key Ministers and Ministries so that the public and the relevant stakeholders can have greater confidence in what the government is thinking and doing to tackle these challenges.

I would be happy to lend my services on a pro-bono basis to any Ministry and Minister including sitting in NACCOL to provide my views and to communicate any government plans which I think are workable to industry groups, business chambers and associations as well as the larger public on the inflation and supply chain challenges which the country is currently facing.