As background, I used to intern for the Monetary Authority of Singapore (MAS) in 1998 during the Asian Financial Crisis. During that time, I wrote a short paper recommending the establishment of a Deposit Insurance Scheme in Singapore similar to the Federal Deposit Insurance Scheme (FDIC) in the United States but customized to the smaller and more stable banking market in Singapore. On this policy, Malaysia’s Deposit Insurance Corporation (MDIC / PDIM) was established in August 2005 which is a few months BEFORE the establishment of Singapore’s DIC in October 2005. In this respect, we were more proactive than Singapore.

I would like to take this opportunity to raise the following questions with regards to the Amendments to the Malaysia Deposit Insurance Corporation Act 2011. Although these questions may be more suited to be brought up during the committee stage of the debate, I would like to give the civil servants more time to prepare the answers to these questions, which is why I am bringing them up now.

1) My first question is with regards to the composition of the Board of Directors of MDIC.

I support Clause 4 of this amendment which is to make clear the expertise and background necessary to be appointed as a member of the BoD of MDIC as well as the appointment of alternate directors if the appointed director is not able to attend the board meetings. The current membership of the BoD of MDIC is indeed impressive and comprises of individuals with relevant experience from both the public and the private sectors. It is also noteworthy that 5 out of the 9 directors are women. But I want to point out that 7 out of the 9 directors are appointed by the Minister of Finance, including the Chairman.

Since MDIC has 42 banks and 50 insurance companies as its members, wouldn’t it be more appropriate for the banking and insurance industry, through their own industry association such as the Association of Banks in Malaysia (ABM), Life Insurance Association of Malaysia (LIFE) and Persatuan Insurans Am Malaysia (PIAM) / General Insurance Association of Malaysia. I am sure there are many retirees with ample experience who have worked as part of the management team in banks and insurance companies who can join the board as industry representatives. They will provide relevant industry insights to regulate the financial sector in Malaysia.[1] Section 11 only states that at least ONE member of the BOD who is appointed by the Minister should have relevant banking and financial sector experience. Given the complexity of both the banking as well as insurance sector (which can be further divided into life and non-life insurance), wouldn’t it be better to increase the number of industry representatives to reflect the financial landscape?

2) My second question is with regards to allowing the corporation to transfer monies from one of the deposit insurance fund to another.

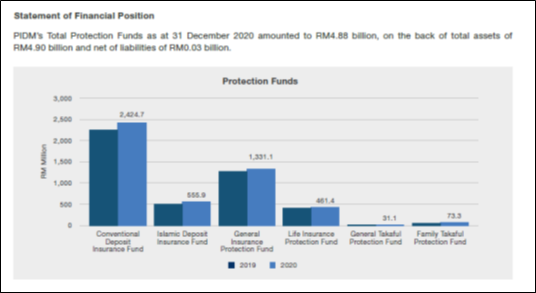

I agree with Clause 9 which is to amend Section 28 of the Act so as to allow greater flexibility to the Corporation to shift monies from one fund to another as and when the need arises. As I understand, there are currently 6 deposit insurance funds which are managed by the Corporation for (i) Islamic Deposits (ii) Conventional Deposits (iii) Family Takaful (iv) General Takaful (v) Life Insurance and (vi) General Insurance. The depletion rate of some of these funds may be faster than others because of possible payouts to different depositors from different sectors of the financial market.

But what is the internal mechanism within the MDIC to analyse and decide on the need to shift these monies from one fund to another? Is there a separate committee apart from the Audit, Governance and Remuneration Committees which has the internal mandate to examine the funding impact associated with shifting monies from one fund to another? I ask the Minister to explain.

3) My third question pertains to the mention of “Business Transfer Schemes” which is a new term introduced in this amendment.

“Business Transfer Scheme” is found in Clause 12 (for the new section 46A), Clause 13 (for the new Section 47 (2)), Clause 17 (for the new section 49A), Clause 23 (for the new Section 71 (3)), Clause 27 ( for the new section 73A). Can the Minister give a specific example of the need to include a business transfer scheme in a bank or insurance company for the purpose of deposit protection? Is this new section / amendment for cases where the bank or insurance company sets up a new subsidiary and transfers part of their existing deposits to this new subsidiary? Or does this amendment take into account Mergers and Acquisition (M&A) activities involving banks and insurance companies? For example, it was announced in June 2021 that Italian insurance company Generali will acquire a majority stake in the AXA AFFIN joint venture and also plans to increase its stake in MPI from 49% to 100%.[2]

[1] Section 14(1)(b) disallows a current employee of any member bank from being a director.

[2] https://www.generali.com/media/press-releases/all/2021/Generali-signs-agreement-in-Malaysia