I had asked the Finance Minister on 13th October 2014 on the reasons why the share price of Felda Global Ventures Holdings Bhd (FGVH) dropped so steeply from its offer price of RM5.39 in 28 June 2012 to only RM3.67 on 11 September 2014. This was despite a record performance by the Kuala Lumpur Composite Index (KLCI) which appreciated from 1599 to 1855 points (16%) over the same period.

In fact, since September, the price has declined further to a low of RM3.24. This represents a shocking 40% decline in its price over just 2 years.

In the relatively lengthy reply provided by the Finance Ministry, the only reason for the poor performance of FGVH was attributed to the drop in the global crude palm oil (CPO) prices which has dropped from approximately US$930 in June 2012 to US$675 today.

However the answer provided by the Ministry was certainly less than honest. If the terrible performance of FGVH was solely attributable to CPO prices, then surely all other plantation companies will be afflicted with the same poor performance.

Over the past 6 months for example, FGVH was the worst performer of all plantation stocks listed on Bursa Malaysia. Based on data as at 15 October 2014, FGVH stock price dropped by 29.1% compared against its peers – IJM Plantations (-6.3%), IOI Corp (-2.7%), Genting Plantatins (-9.4%) and Sime Darby (-1.6%). The closest poor performer was KL Kepong whose price dropped by 16.6% over the same period.

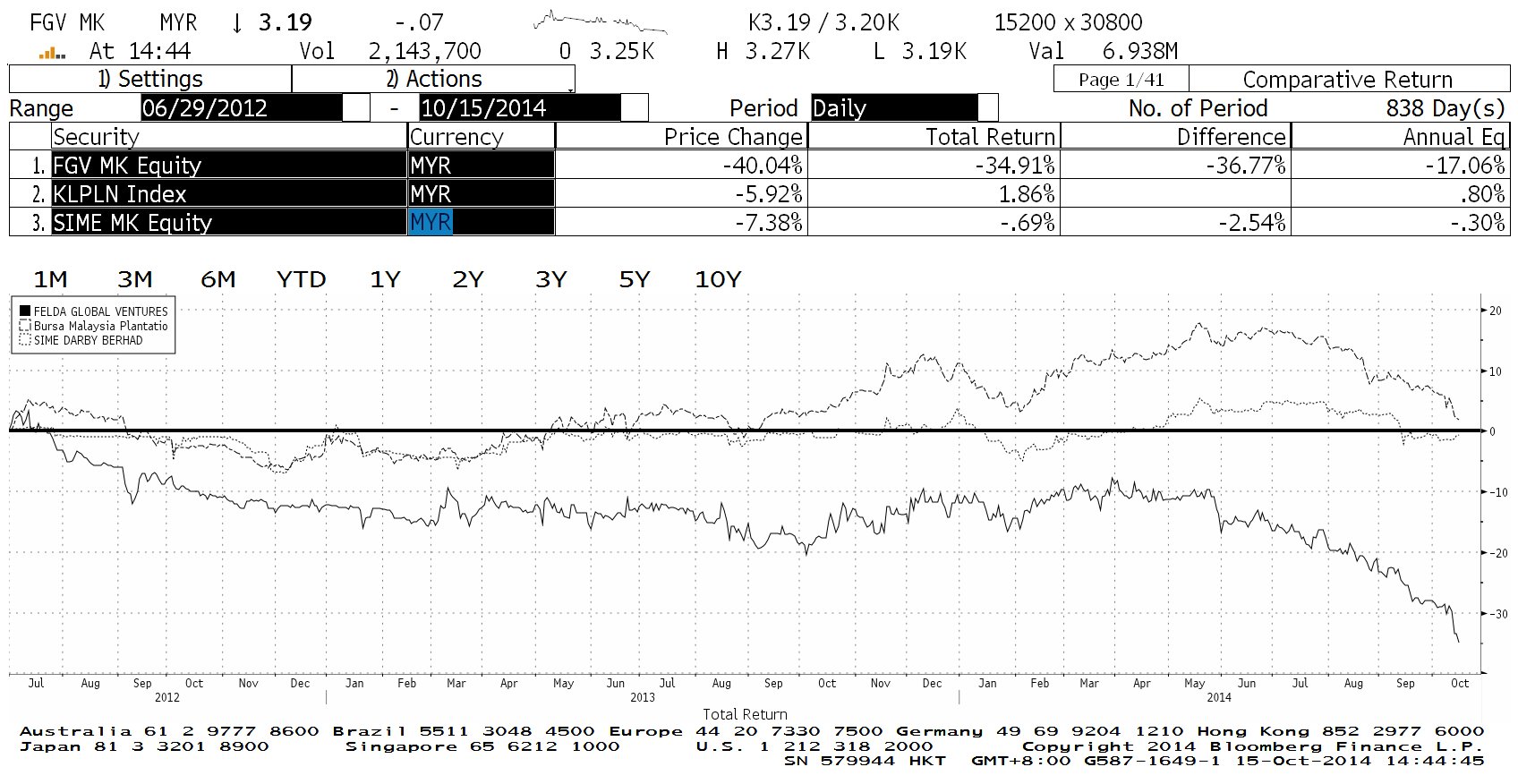

Not only was FGVH a terrible stock to own over the past 6 months, it was a consistent under-performer within any measurable period ever since its listing on the stock exchange.

I’ve attached a chart captured from Bloomberg which compared FGVH performance from the date of listing to 15th October 2014 with Sime Darby Bhd, benchmarked against the Bursa Malaysia Plantation Index. While Sime performed 2.54% below its market peers, FGVH underperformed by 36.77%.

{kind=link}

The embarrassing performance by FGVH was despite the solid support by government related funds such as the Employees Provident Fund (KWSP), the Pensions Fund (KWAP), Lembaga Tabung Haji as well as state funds.

KWSP for example, has increased its initial 5% investment in FGVH at listing date to in excess of 8% today. Based on its initial 5% holdings alone, the losses accumulated in FGVH shares would have amounted to RM255.4 million. Similarly, KWAP and Tabung Haji which own a 7% and 7.8% stake in FGVH, would have lost RM357.5 million and RM398.4 million respectively.

The Chairman of FGVH, Tan Sri Isa Samad together with the top management of the company must take collective responsibility in the poor performance of the company. This is especially since FGVH in its 2012 Annual Report boasted that “FGVH’s stunning debut on the main market in Bursa Malaysia in 2012 was a global sensation. This is just the start of our metamorphosis into a global powerhouse.” The performance of FGVH over the past 2 years only made the above statement a laughing stock, for not only did the company fail to become a “global powerhouse”, it was a trailing laggard even in Malaysia.

Dato’ Seri Najib Razak, as both the Finance and Prime Minister, who promised Felda settlers the stars during the listing exercise must therefore take decisive action to reverse the decline in the company, before the rot continues and becomes irreversible.