Another RM45 billion fund injection as an economic stimulus may cause our fiscal deficit to widen to 9% of GDP but will allow Malaysia to quickly come out of the COVID-19 economic recession. Malaysia’s GDP contraction of 17.1% in the second quarter is the worst in ASEAN. An additional RM45 billion similar to the one in April, is urgently needed to put our economy back on track to save businesses and jobs.

Thailand, which depended nearly 2 times more heavily on tourism than Malaysia, just announced a smaller than expected GDP 2nd quarter growth contraction of 12.2%. If the Federal government continues to adopt a lackadaisical attitude that the economy will right itself, then we are in for a rude shock for the remainder of the year.

Year-on-year GDP growth of major Asean economies

| Economies | First quarter GDP Growth | Second quarter GDP growth |

| Malaysia | 0.7% | -17.1% |

| Indonesia | 3.0% | -5.3% |

| Philippines | -0.2% | -16.5% |

| Singapore | -0.3% | -13.2% |

| Thailand | -1.8% | -12.2% |

| Vietnam | 3.8% | 0.4% |

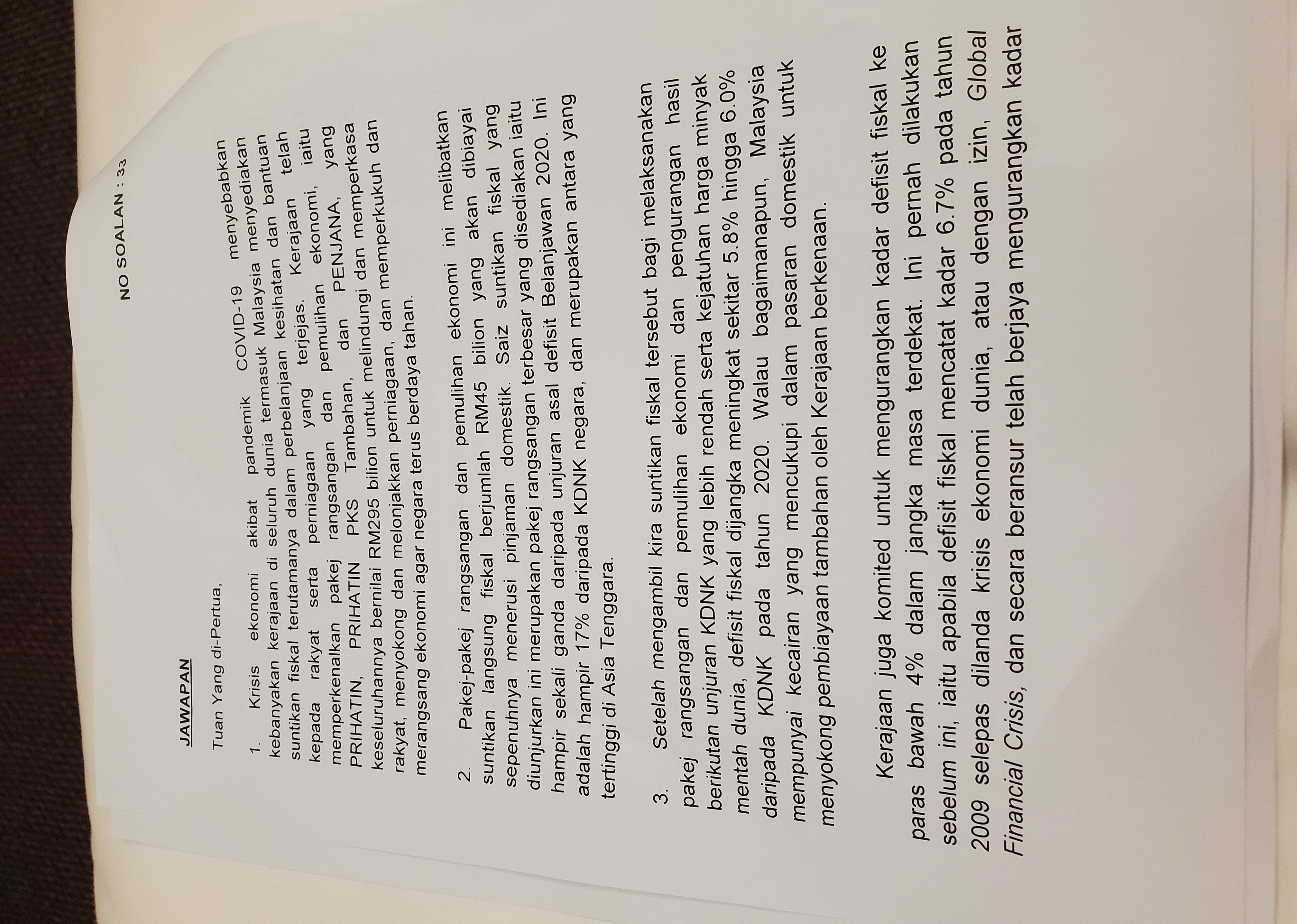

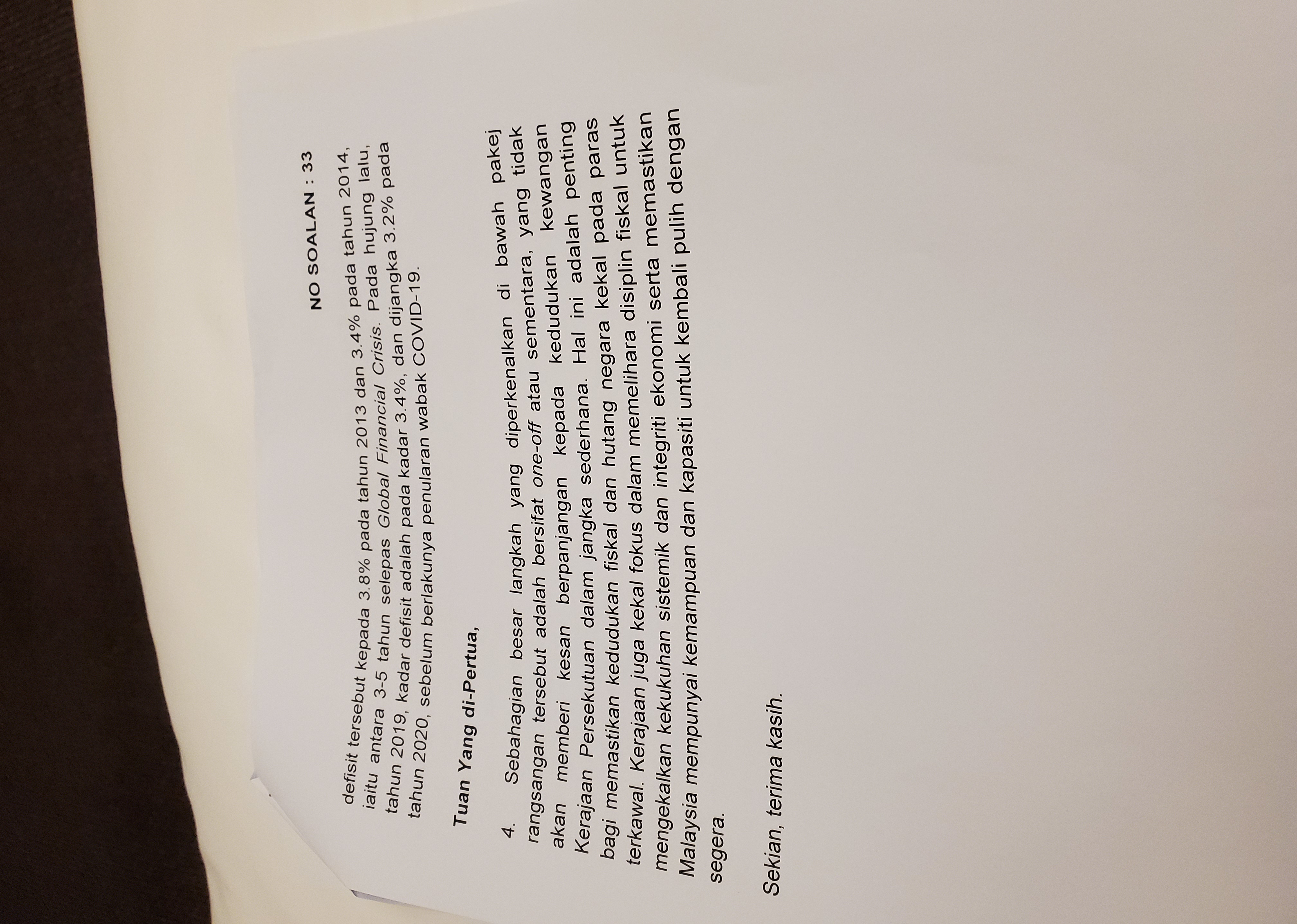

Based on Finance Ministry’s figures of a 5.8% to 6% deficit to GDP(see Parliament’s answer attached) for this year, I would project that an additional RM45 billion fund injection would cause the deficit to rise to 9% of GDP. A deficit of 9% of GDP would be tolerable to save people’s lives by rescuing their businesses and jobs. 9% deficit to GDP is not the worst numbers on record. Malaysia’s worst deficit to GDP was in 1982, at 16.6% and in 1981, at 15.6% of GDP.

Even government backbenchers are not convinced by the government’s political spin, because economic data shows the government has not been doing enough to mitigate the recession. Despite the RM45 billion fund injection, Bank Negara Malaysia’s data shows the government’s second quarter operating expenditure fell 2.1% from a year ago, compared to a 5.2% increase in the first quarter.

Further, the government can rely on borrowings from the domestic market as they have done for the initial RM45 billion fund injection(see parliamentary answer attached). As at end-June 2020, the local bond market size was RM1.6 trillion (including government bond, corporate bond and BNM papers). A domestic RM45 billion debt issuance would be easily absorbed and digested.